: Which Wins in 2026?")

I still remember sitting at my desk during my first week at a “real” corporate job, staring blankly at the benefits enrollment screen on my laptop.

Table Of Content

- The Core Mechanic: When Do You Want to Pay the IRS?

- The Traditional 401(k): Get the Tax Break Today

- The Roth 401(k): Get the Tax Break Tomorrow

- The Break-Even Tax Rate Framework

- When the Traditional 401(k) Is the Clear Winner

- When the Roth 401(k) Is the Clear Winner

- The 2026 Game Changer: The High-Earner Roth Mandate

- The Match Is Always Pre-Tax (You’ll Have Both Anyway)

- State Taxes: The Sneaky Wealth Killer

- My Personal Decision Tree: How I Choose

- The Bottom Line

- FAQ: Roth vs. Traditional 401(k) in 2026

I had carefully picked my contribution percentage. I had agonized over my investment funds. And then, right at the bottom of the page, there was a little toggle switch that stopped me in my tracks: Traditional or Roth?

I had absolutely no idea what it meant. I leaned over and asked a coworker what he did. He shrugged, didn’t look up from his monitor, and said, “I think Roth is better because it’s tax-free later.”

That sounded good enough to me. I clicked Roth, closed the laptop, and went back to work.

Over the years, as I started taking my own portfolio seriously and actually managing my money, I realized just how much that five-second blind guess was costing me. Choosing between a Roth and a traditional 401(k) is not a coin flip. It is not a personality test. And it is definitely not something you should base on a watercooler chat.

It is a strategic math problem.

As we move into 2026, the government has actually changed the rules of the game specifically for higher earners making this decision more complicated and more important than ever.

Today, I want to walk you through exactly how I look at the Roth vs. traditional 401(k) debate. I am not going to give you generic “it depends” advice or bury you in accounting jargon. Instead, I am going to share the clear, practical framework you can use to figure out which account actually puts more money in your pocket over your lifetime.

The Core Mechanic: When Do You Want to Pay the IRS?

Before we get into the heavy strategy and the new 2026 rules, we need to clear up how these two accounts actually function.

In 2026, the IRS allows you to contribute up to $24,500 of your own salary into your workplace 401(k). That is your base limit. But the IRS, as always, wants its cut of your income. The only real difference between a traditional 401(k) and a Roth 401(k) is when you write that check to the government.

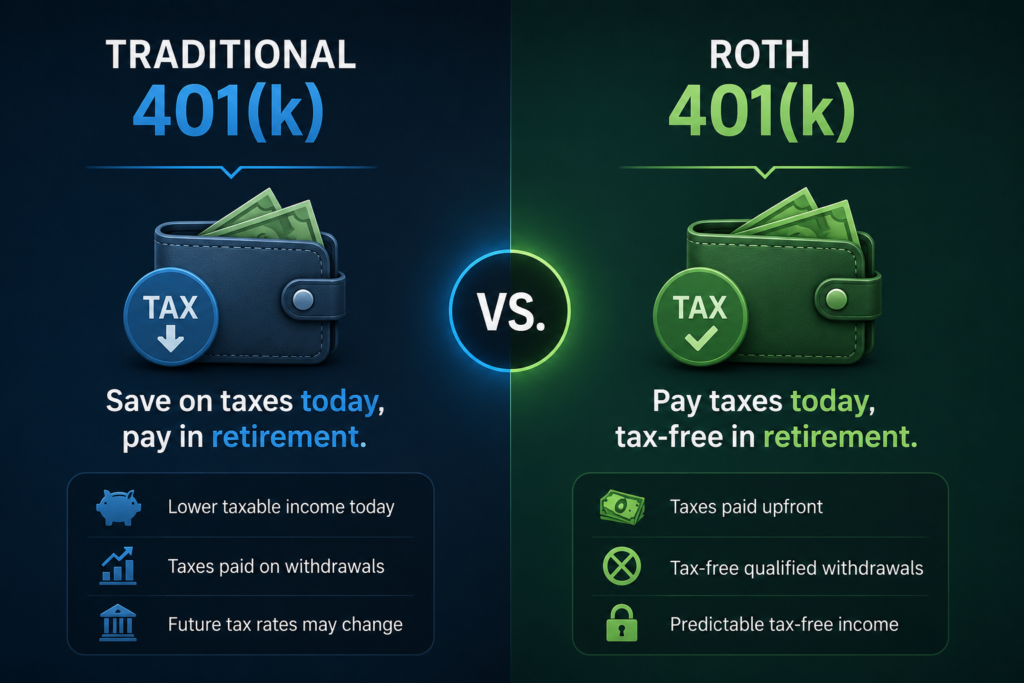

The Traditional 401(k): Get the Tax Break Today

When you put money into a traditional 401(k), you are using pre-tax dollars. The government is essentially rewarding you for saving by lowering your tax bill right now.

Let’s say you earn $100,000 a year, and you decide to contribute $10,000 to a traditional 401(k). When tax season rolls around, the IRS pretends you only earned $90,000 that year. You get an immediate, guaranteed tax deduction.

That money goes into your account and grows completely tax-free for decades. You can buy, sell, and rebalance funds inside the account without triggering a single taxable event.

However, the bill eventually comes due. When you are 65 and you pull that money out to pay for groceries, a new car, or a vacation, the IRS treats every single dollar you withdraw as ordinary income. You will pay taxes on it based on whatever your tax bracket is in that future year.

The Roth 401(k): Get the Tax Break Tomorrow

When you put money into a Roth 401(k), you are using after-tax dollars. You are choosing to pay your income taxes up front, today.

Using that same $100,000 salary, if you contribute $10,000 to a Roth 401(k), you are still taxed on your full $100,000 income this year. There is no immediate deduction. You feel the pain of those taxes immediately in your paycheck.

But here is where the magic happens. Just like the traditional account, the money grows tax-free for decades. The massive difference is that when you pull the money out in retirement, you owe absolutely zero taxes. The growth, the original contributions, all of it is completely yours. The IRS cannot touch it.

The Break-Even Tax Rate Framework

When I first started investing, I honestly thought the Roth 401(k) was the ultimate financial cheat code. Tax-free growth for thirty years? Why would anyone, ever, in their right mind, pass that up?

What finally made this click for me was learning about the break-even tax rate.

The mathematical reality which surprises almost everyone I talk to is this: If your marginal tax bracket remains exactly the same today as it is in retirement, a traditional 401(k) and a Roth 401(k) will leave you with the exact same amount of spendable money.

Let that sink in for a second.

If the tax rate doesn’t change, the final outcome doesn’t change. Taking a 24% tax hit today on a small amount of money (Roth) leaves you with the exact same net wealth as taking a 24% tax hit decades from now on a much larger, compounded amount of money (Traditional). The math is perfectly identical.

So, the entire debate is actually incredibly simple. It hinges on one single question: Do you think your tax rate is higher today, or will it be higher in retirement?

When the Traditional 401(k) Is the Clear Winner

If you are currently in your peak earning years, pulling down a high salary, you are likely sitting in a high tax bracket. Let’s say you are in the 24%, 32%, or even 35% federal bracket.

When you retire, you stop working. Your W-2 income drops to zero. You will likely be living off a combination of your portfolio withdrawals and Social Security. Because your income is generally lower in retirement than during your peak career years, your tax bracket will likely be much lower perhaps 12% or 22%.

In this scenario, paying a 32% tax today to fund a Roth 401(k) is a massive, wealth-destroying mistake.

You should absolutely use a traditional 401(k). You take the massive 32% tax deduction right now, let the money compound, and then pay taxes at a much lower 12% or 22% rate when you withdraw the money as an older adult.

When the Roth 401(k) Is the Clear Winner

On the flip side, let’s say you are young, just starting your career, taking a gap year, or currently working in a lower-paying entry-level job. You are likely in a low tax bracket, such as 10% or 12%.

You expect your career to take off. You expect your salary to grow dramatically over the next few decades, and you expect to have a substantial amount of taxable income in retirement.

In this scenario, paying a 12% tax today is an absolute bargain.

You should lock in that ridiculously low tax rate now by funding a Roth 401(k). You pay the tiny tax bill today, let the money grow, and pull it out entirely tax-free when you are wealthy and sitting in a much higher bracket later in life.

The 2026 Game Changer: The High-Earner Roth Mandate

Now, here is where things get really interesting, and why you need to pay close attention to your pay stubs this year.

Starting in 2026, the government has essentially taken this choice away from a very specific group of people.

If you are 50 or older, the IRS allows you to make “catch-up” contributions to your 401(k) to help you supercharge your savings before you stop working. For 2026, that means you can put in an extra $8,000 on top of the standard $24,500 limit. And if you happen to hit the very specific age window of 60 to 63, you get a special “super” catch-up limit of $11,250.

But a new rule under the SECURE 2.0 Act has just taken effect for 2026, and it carries a massive sting for high earners.

If your wages subject to FICA taxes were over $150,000 in the previous calendar year, all of your catch-up contributions must be made to a Roth account.

Let me repeat that: You are no longer allowed to take a pre-tax deduction on your catch-up money if you earn over $150,000.

I’ve been talking to a lot of investors who are completely blindsided by this. As we just established in the break-even framework, high earners typically prefer traditional 401(k)s precisely because their tax bracket is so high right now. Being forced to push $8,000 to $11,250 into a Roth means losing a valuable tax deduction, which directly results in a larger tax bill this year.

If you fall into this high-earner bucket, you need to prepare for your paycheck to look a little smaller as those post-tax deductions hit.

Worse, if your employer’s plan hasn’t updated its payroll systems to offer a Roth option yet, you might be temporarily blocked from making catch-up contributions entirely until their administrative team fixes it. Keep a very close eye on your HR portal this year.

The Match Is Always Pre-Tax (You’ll Have Both Anyway)

One of the most common misconceptions I hear comes from people who proudly tell me, “I am 100% Roth. I don’t want to deal with taxes at all in retirement.”

I hate to break it to you, but unless you own the business, you probably aren’t 100% Roth.

If your company offers a 401(k) match, that matched money is almost always deposited as pre-tax, traditional money. Even if every single dollar you contribute out of your own paycheck goes into the Roth side of the account, your employer’s contribution is going into the traditional side.

This means that by the time you retire, you are going to have a mixed portfolio regardless of what you chose on that enrollment screen.

And honestly? I personally love this. Having both pre-tax and post-tax money in retirement is like having different levers you can pull to control your tax bracket.

If pulling out more traditional money in a specific year is going to push you up into a painfully high tax bracket, you can simply stop, pivot, and pull your remaining living expenses from your Roth account instead. We call this “tax diversification,” and it is an incredibly powerful tool for protecting your wealth later in life.

State Taxes: The Sneaky Wealth Killer

When we talk about tax brackets and retirement planning, almost everyone hyper-focuses on federal taxes. But where you live right now and where you plan to live when you retire can completely rewrite the math on the Roth vs. traditional debate.

Let’s say you currently live and work in California, New York, or New Jersey. These states are notorious for their painfully high state income taxes. If you fund a Roth 401(k) today, you are paying heavy federal taxes plus heavy state taxes on that money right now.

But what if your grand retirement plan involves moving to Florida, Texas, or Nevada? Those states have zero state income tax.

If you use a traditional 401(k) today, you get to deduct your contributions and completely avoid paying those high New York or California state taxes while you are working. Then, you move to Florida, pull the money out, and pay absolutely zero state tax on the withdrawal. You have effectively bypassed state income taxes on that money forever. This is geographic arbitrage at its finest.

On the flip side, if you currently live in Texas (paying no state tax) but you plan to retire on a beach in California, a Roth 401(k) becomes incredibly attractive. You’d pay the low taxes in Texas today, lock the money away, and avoid the high California taxes when you withdraw it later.

My Personal Decision Tree: How I Choose

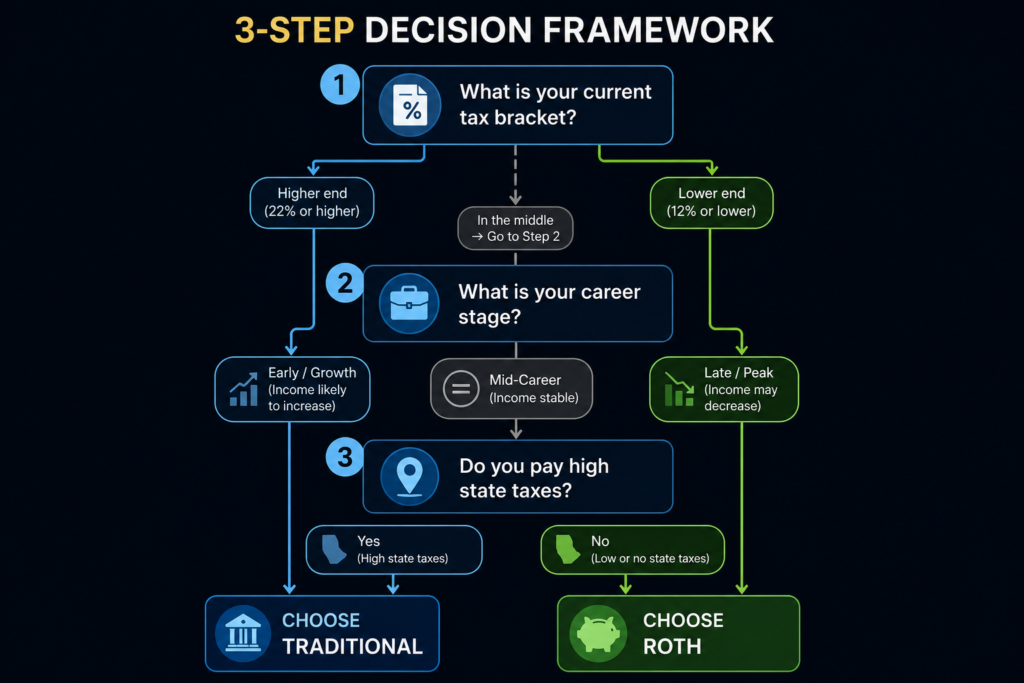

If you are still feeling stuck, I get it. It can feel overwhelming. To simplify things, this is the exact three-question checklist I run through in my own portfolio every single year when deciding how to direct my contributions.

1. What is my marginal tax bracket today? If I am in the 24% bracket or higher, I heavily favor the traditional 401(k). That immediate tax savings is a guaranteed return on my money right now, and I assume my taxes will be lower in retirement. If I am in the 10% or 12% bracket, I am jamming every spare dollar I can find into the Roth.

2. Where am I in my career trajectory? If I just got promoted to a senior role and I am earning more money than I ever have in my life, the traditional account is my best friend. If I am taking a sabbatical, starting a brand new business with low initial income, or in an entry-level role, I am locking in the Roth.

3. What does my future state tax situation look like? If I am living in a high-tax state but dreaming of a low-tax retirement state, the traditional 401(k) gets a massive bonus point in my calculation.

The Bottom Line

I spent way too much time in my twenties agonizing over whether I made the “wrong” choice by clicking Roth instead of traditional on that HR portal.

I’ve learned that the only truly wrong choice is getting paralyzed by the decision and choosing not to contribute at all.

Whether you pay taxes now or pay them later, the single most important factor in your retirement success is the compound interest you build over decades of consistent, relentless investing. Use the break-even framework, pay attention to the new 2026 FICA rules if you are a high earner, and make the best mathematical decision you can with the information you have today.

Your future self will thank you for simply staying in the game.

FAQ: Roth vs. Traditional 401(k) in 2026

Can I contribute to both a Roth and a traditional 401(k) in the same year? Yes, absolutely. You can split your contributions however you want. You could do 50% traditional and 50% Roth, or 80/20. You just have to ensure that your total combined contributions do not exceed the 2026 limit of $24,500.

Does a Roth 401(k) have income limits like a Roth IRA? No, and this is a massive benefit. High earners are barred from contributing directly to a Roth IRA once their income passes a certain threshold. However, there are absolutely no income restrictions for contributing to a Roth 401(k) through your employer.

Are Roth 401(k) accounts subject to Required Minimum Distributions (RMDs)? No. Thanks to recent changes in retirement law, you are no longer forced to take RMDs from a Roth 401(k) during your lifetime. Traditional 401(k)s, however, still require you to take minimum distributions once you reach a certain age.

: Which Wins in 2026?")

: Which Wins in 2026?")

vs. IRA vs. Roth IRA: The Complete 2026 Priority Order")

No Comment! Be the first one.