I remember exactly what it felt like when I first started trying to grow my money. I opened my first brokerage account, transferred over a chunk of my hard-earned savings, and immediately felt completely overwhelmed. The screen was flashing green and red, financial news was screaming about impending market crashes, and thousands of different stocks were begging for my attention.

Table Of Content

Like a lot of beginners, I made the mistake of thinking that complex problems require complex solutions. I bought a handful of individual tech stocks because I liked their products. I bought a specialized clean energy fund because I read a compelling article about it. I even tried timing the market, holding cash when I got nervous and buying when I felt optimistic.

The result? I was checking my phone a dozen times a day, losing sleep over market dips, and entirely failing to beat the average market returns. I was exhausted. I realized I didn’t want a second job as a frantic day trader; I just wanted to build wealth quietly and reliably.

What finally made this click for me was discovering a strategy so brilliantly boring that it almost felt like I was doing something wrong. It’s a strategy championed by financial legends like Jack Bogle, and it completely changed my life. It’s called the 3-fund portfolio.

If you want to stop gambling with your savings and start investing like a professional, this is exactly how I look at it.

The Anatomy of a 3-Fund Portfolio

When we strip away all the financial jargon, investing is simply buying small pieces of businesses and lending money to institutions. The 3-fund portfolio takes this concept to its absolute most efficient extreme.

Instead of trying to find the needle in the haystack by picking the next Apple or Amazon, this strategy buys the entire haystack. It uses three broad index funds to give you ownership of nearly every publicly traded company in the world, plus a steady foundation of bonds to keep the ride smooth.

An index fund, if you aren’t familiar, is just a basket of investments that tracks a specific market. Instead of paying a high-priced Wall Street manager to guess which stocks will go up, an index fund buys everything on the list. Because there’s no expensive manager to pay, the fees are practically zero.

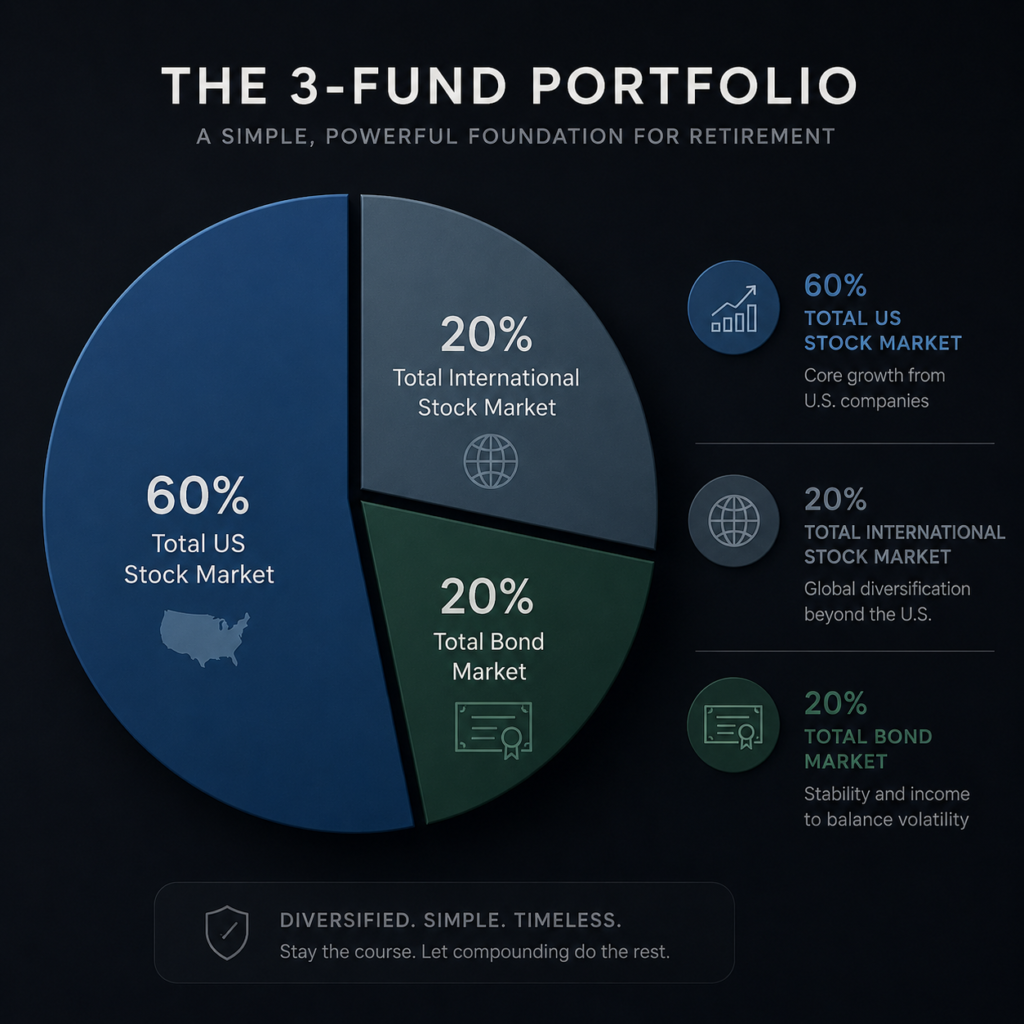

The three components of this portfolio are beautifully simple.

First, there is the Total US Stock Market Index. This is the engine of your portfolio. When you buy a fund like this, you are buying a tiny slice of thousands of companies across the United States. You own pieces of the massive tech giants, the regional banks, the airlines, the pharmaceutical companies, and the small businesses just starting to break out. If the US economy grows, this fund grows.

Second, there is the Total International Stock Market Index. I personally avoid putting all my eggs in one geographic basket. The US has had an incredible run over the last decade, but history shows us that international markets and the US market take turns outperforming each other. By holding an international index fund, you capture the growth of companies in Europe, Asia, emerging markets, and beyond. You own the world.

Third, there is the Total Bond Market Index. If stocks are the engine of your portfolio, bonds are the shock absorbers. Stocks are volatile; they can drop 20% or 30% in a bad year. Bonds are essentially loans you make to governments and highly rated corporations. They pay you a steady interest rate and are generally much more stable than stocks. When the stock market crashes, bonds are what keep you from panicking and selling everything at a loss.

Why This Strategy Beats the Alternatives

It is incredibly tempting to think you can outsmart the market. We all want to be the person who bought Bitcoin in 2013 or Tesla before it skyrocketed. But I’ve learned the hard way that picking individual stocks is a loser’s game for the vast majority of us.

Even professional mutual fund managers—people who went to Ivy League schools, work 80 hours a week, and have millions of dollars in research software—rarely beat a simple index fund over a ten-year period. If the professionals can’t consistently beat the market, we shouldn’t expect to do it on our lunch break.

The 3-fund portfolio works because it relies on the undeniable long-term growth of the global economy, not the unpredictable success of a single company. You completely eliminate “single company risk.” If one massive corporation goes bankrupt tomorrow, your portfolio will barely feel a ripple because that company represents a fraction of a percent of your total holdings.

Beyond diversification, the true secret weapon of the 3-fund portfolio is its cost.

When I first started investing, I had no idea how destructive fees could be. If you invest in a traditional mutual fund managed by a person, they might charge you a 1% fee every year. That sounds tiny, right? It’s not. Over thirty years, that 1% fee can eat up hundreds of thousands of dollars of your potential wealth. It completely cannibalizes your compound interest.

Because the 3-fund portfolio uses passive index funds (or ETFs, which act similarly), the fees are virtually zero. You keep the money your money makes. That alone is a massive mathematical advantage over traditional investing.

Setting Your Asset Allocation

The most common question I get when explaining this is, “Okay, I buy these three funds, but how much of each do I buy?”

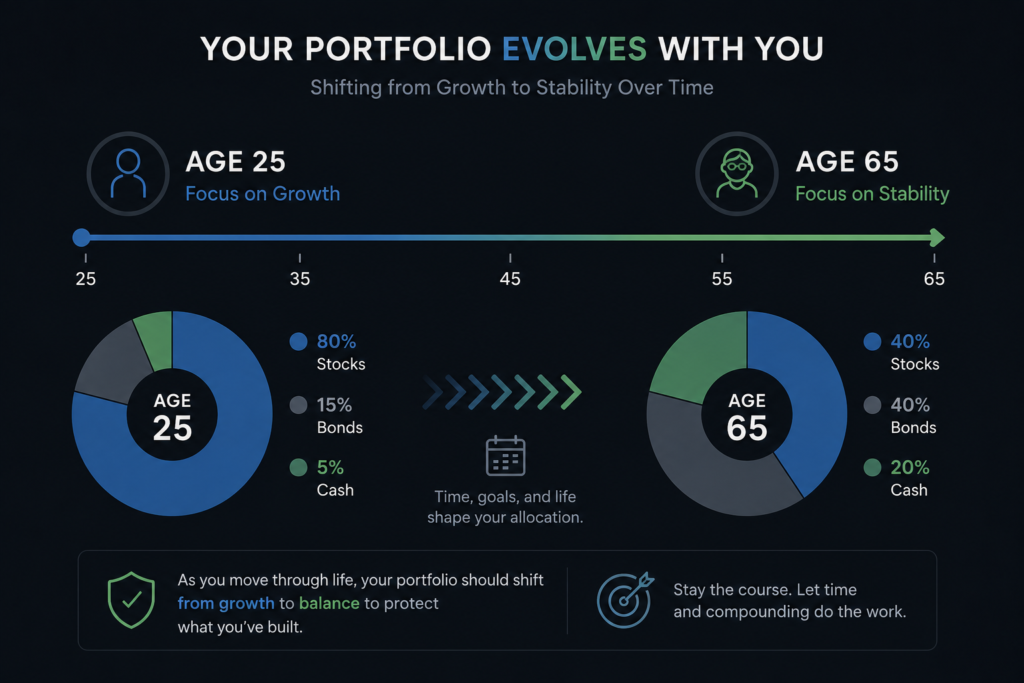

This is called your asset allocation, and it is the single most important decision you will make. Your allocation determines both your potential returns and your level of risk. There is no one-size-fits-all answer here, because your allocation needs to match your age, your goals, and—most importantly—your ability to sleep at night when the market drops.

Let’s break down how to think about this.

The younger you are, the more risk you can afford to take. If you are in your twenties or thirties, you have decades before you need this money. You actually want the market to drop occasionally so you can buy more shares at a discount. Therefore, your portfolio should be heavily weighted toward stocks.

A common aggressive allocation for a young investor might be 80% or 90% in stocks, split between US and International, with only 10% to 20% in bonds. Some young investors even choose to skip bonds entirely, though I personally like having a small bond allocation to act as “dry powder” to buy stocks during a crash.

As you get closer to retirement, your priorities shift. You are no longer solely focused on growing your wealth; you become intensely focused on protecting it. You don’t have the time to wait out a five-year market recovery. This is when you start shifting your percentages, selling some of your stocks and buying more bonds to stabilize your nest egg. A retiree might hold 60% in bonds and only 40% in stocks.

In my own portfolio right now, I use a fairly aggressive split. I hold roughly 60% in a Total US Stock Market fund, 20% in a Total International Stock Market fund, and 20% in a Total Bond Market fund. This gives me a strong growth engine with enough international diversification to feel safe, and just enough bonds to soften the blow when the inevitable recession hits.

How to Actually Buy the Funds

One of the best things about this strategy is that you can build it at almost any major brokerage. Vanguard, Fidelity, and Charles Schwab are all excellent, low-cost platforms that I trust. I personally use Vanguard because they essentially invented the index fund, but you cannot go wrong with any of the top three.

To make this practical, let’s look at exactly what you would type into the search bar at these brokerages.

If you use Vanguard, your three funds might be VTSAX (Total US Stock Market), VTIAX (Total International Stock Index), and VBTLX (Total Bond Market Index). These are mutual funds, but Vanguard also offers equivalent ETFs like VTI, VXUS, and BND if you prefer to trade them like stocks.

If you are at Fidelity, you might use their “Zero” funds, which literally charge zero fees. Your setup would be FZROX (Total US), FZILX (Total International), and FXNAX (Total Bond).

The mechanics are incredibly simple. You deposit money into your account. You determine your percentages. Then you buy the funds. If you have $1,000 to invest and want a 60/20/20 split, you buy $600 of the US fund, $200 of the International fund, and $200 of the Bond fund. That’s it. You are now a globally diversified investor.

The Art of Doing Nothing

Here is where the 3-fund portfolio gets difficult. The hardest part isn’t setting it up; the hardest part is leaving it alone.

When you manage your own money, human psychology becomes your absolute worst enemy. The news cycle is designed to keep you terrified. You will hear about impending economic doom, inflation crises, and geopolitical disasters. Your friends might brag about how much money they made on a random crypto coin. You will feel an intense urge to tinker with your portfolio, to sell before a crash, or to chase the latest hot sector.

Do not do it.

I have watched brilliant people destroy their wealth simply because they couldn’t sit on their hands. Tinkering destroys returns. When you sell out of fear, you lock in your losses. When you try to time the market, you inevitably miss the best days of recovery, which is when the real wealth is made.

With a 3-fund portfolio, your job is mostly to ignore it. Automate your contributions so money moves from your checking account into your three funds every single month, regardless of what the market is doing. Whether the market is at an all-time high or an all-time low, you just keep buying. Over decades, this relentless, mechanical purchasing is what builds generational wealth.

Rebalancing: Your Once-a-Year Maintenance

There is only one active task you need to do to maintain this strategy, and it takes about fifteen minutes a year. It’s called rebalancing.

Because your three funds will grow at different rates, your target percentages will drift over time. Let’s say you started with my allocation: 60% US stocks, 20% International, 20% Bonds. Now imagine the US stock market has an incredible, booming year. Because your US fund grew so much faster than your bonds, your portfolio might now look like 70% US stocks, 15% International, and 15% Bonds.

Your portfolio has become riskier than you intended because stocks now make up a much larger portion of the pie.

To fix this, you rebalance. You log in, sell a little bit of your overperforming US stock fund, and use that cash to buy more of your underperforming international and bond funds until you are back to your 60/20/20 target.

This process forces you to do the one thing every investor knows they should do but rarely actually does: sell high and buy low. You are automatically trimming your winners and buying your losers on sale. I usually pick one day a year—like my birthday or a random day in January—to log in, check my percentages, rebalance if necessary, and then log back out for another 364 days.

My Final Takeaway

Investing doesn’t have to be your hobby. In fact, it shouldn’t be.

When I stopped trying to beat the market and embraced the boring predictability of the 3-fund portfolio, everything changed. My returns stabilized, my fees plummeted, and most importantly, I got my time back. I stopped reading stock charts and started focusing on my career, my family, and things I actually enjoy doing.

The financial industry spends billions of dollars every year trying to convince you that investing is a highly complex puzzle that only they can solve for you (for a hefty fee, of course). It just isn’t true. By owning the whole world, keeping your fees near zero, and having the discipline to stay the course through market storms, you will outperform the vast majority of investors.

Set up your three funds, automate your monthly contributions, check in once a year, and let the quiet power of compound interest do the heavy lifting for you.

: Which Wins in 2026?")

vs. IRA vs. Roth IRA: The Complete 2026 Priority Order")

No Comment! Be the first one.